How a Correlation Index at Extreme Lows Can Impact Stocks

Source Entity

Yahoo Finance

An analysis of the Cboe 3-Month Implied Correlation Index (Cor3M), explaining how extreme lows in expected stock correlation signal specific market dynamics and impact investment strategies.

Understanding the Cboe 3-Month Implied Correlation Index (Cor3M)

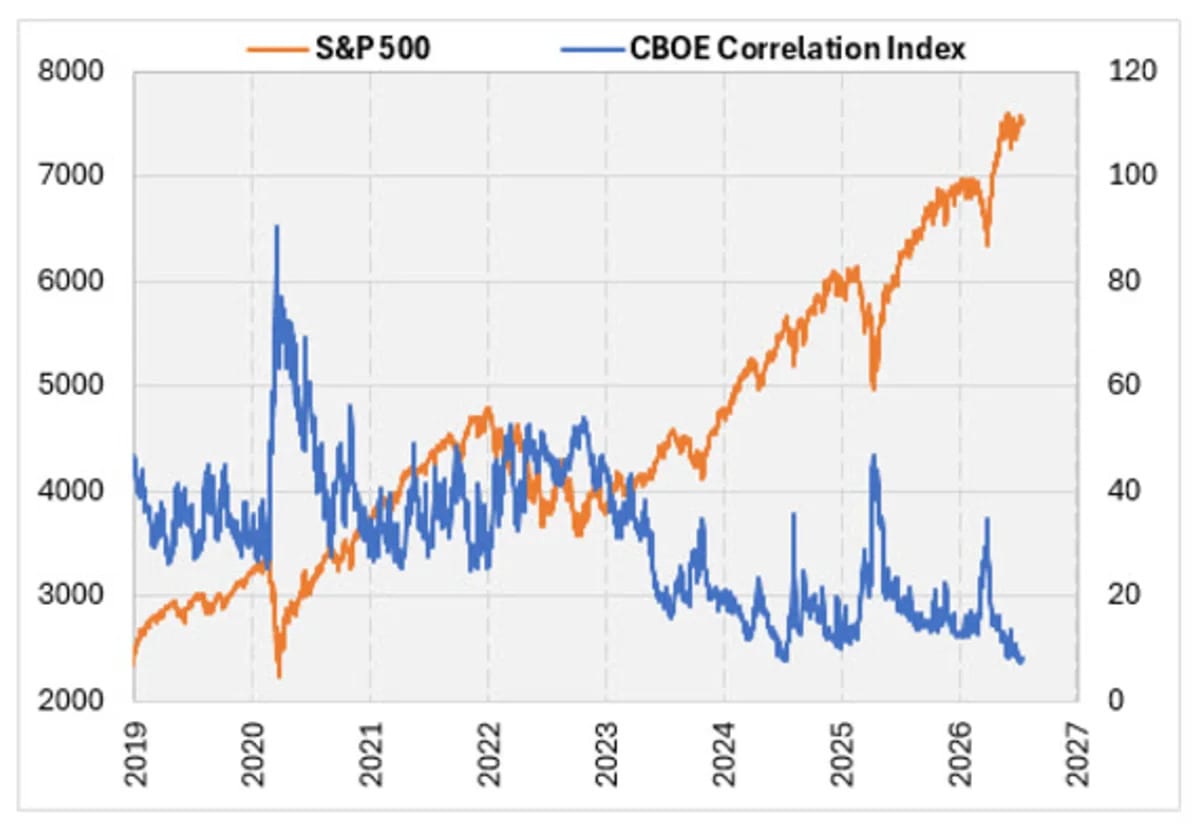

The Cboe 3-Month Implied Correlation Index, commonly referred to as Cor3M, serves as a sophisticated barometer for market sentiment, specifically measuring the expected correlation among S&P 500 stocks over the subsequent three months. Unlike realized correlation, which looks backward at how stocks actually moved, the Cor3M is a forward-looking indicator derived from the pricing of index options and individual stock options. When this index is at extreme lows, it suggests that the market anticipates a period where individual stock movements will be driven more by company-specific fundamentals rather than broad macro-economic trends that push the entire market in a single direction.

The Mechanics of Implied Correlation

To understand the impact of Cor3M, one must distinguish between systemic risk and idiosyncratic risk. High correlation typically occurs during market crashes or systemic shocks, where investors panic and sell all assets regardless of individual quality, leading to a 'correlation of one.' Conversely, when the Cor3M reaches extreme lows, it indicates a shift toward idiosyncratic risk. In this environment, the market expects a 'stock-picker's market,' where the divergence between winning and losing stocks increases. This divergence is critical for active managers who seek to outperform the benchmark by selecting specific equities that can thrive independently of the broader index's trajectory.

Implications of Extreme Lows on Portfolio Diversification

From a strategic standpoint, extreme lows in the Cor3M are highly significant for portfolio diversification. Diversification is most effective when assets have low or negative correlation; if all stocks move in lockstep, diversification provides little protection against a downturn. When Cor3M is exceptionally low, it signals a window where diversification is functioning at its peak efficiency. Investors can potentially reduce their overall portfolio volatility because a decline in one sector or stock is less likely to be mirrored across the rest of their holdings. This creates an opportunistic environment for rebalancing and tactical asset allocation.

Historical Context and Market Behavior

Historically, periods of extreme low correlation often precede shifts in market leadership or volatility spikes. When the market becomes too complacent—evidenced by extremely low implied correlation—it can sometimes signal an underestimation of systemic risk. In many market cycles, a prolonged period of low correlation is eventually interrupted by a catalyst that forces stocks to move together again. Analyzing the Cor3M allows traders to gauge whether the current market stability is based on genuine fundamental divergence or a dangerous lack of perceived risk, providing a layer of psychological insight into the collective mindset of institutional investors.

Predictive Trends for Traders and Investors

Looking forward, the behavior of the Cor3M can help predict the efficacy of various hedging strategies. For instance, when correlation is low, hedging a portfolio using a broad index put option may be less effective than hedging via individual stock options or sector-specific instruments. As the Cor3M fluctuates, traders may shift their focus from 'beta' (market exposure) to 'alpha' (skill-based returns). If the index remains at extreme lows, we can expect continued volatility in individual stock earnings reports to have a more pronounced effect on those specific shares without necessarily dragging down the entire S&P 500.

Summary of Market Impact

In conclusion, the Cboe 3-Month Implied Correlation Index is an essential tool for understanding the internal structure of market risk. Extreme lows in the Cor3M highlight a market environment characterized by individual stock autonomy and high diversification potential. While this allows for greater potential in active stock selection, it also requires investors to be vigilant about the eventual return to higher correlation, which typically accompanies periods of heightened systemic stress. By monitoring the Cor3M, market participants can better align their risk management strategies with the expected behavior of the equity markets.