Bandhan Bank Raises FD Rates on select tenures as Banks Compete for Retail Deposits

Source Entity

Latest News: Today's Latest News Headlines from India & World | Hindustan Times | Hindustan Times

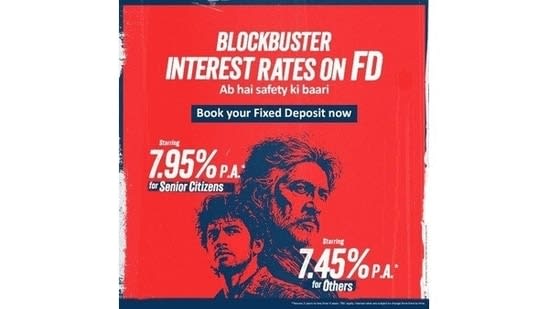

Bandhan Bank has increased its Fixed Deposit (FD) rates, offering 7.45% for general customers and 7.95% for senior citizens on select tenures to enhance its retail deposit base amidst stiff competition from other banks.

Strategic Shift: Bandhan Bank's Push for Retail Deposits

Bandhan Bank has recently announced an upward revision of its Fixed Deposit (FD) rates, targeting specific tenures to attract a broader base of retail depositors. By offering 7.45% for general customers and a premium rate of 7.95% for senior citizens, the bank is positioning itself aggressively in a market where liquidity management has become a primary concern for financial institutions. This move is not merely a routine adjustment but a strategic response to the tightening competition for low-cost and stable funding within the Indian banking ecosystem.

Analyzing the Rate Structure and Target Demographics

The distinction between the rates offered—7.45% for the general public and 7.95% for senior citizens—highlights the bank's focus on a risk-averse demographic. Senior citizens typically seek guaranteed returns and capital preservation, making them the ideal target for higher-yield FDs. By providing a 50-basis point premium, Bandhan Bank is attempting to capture a significant portion of retirement savings, which provide a stable, long-term source of funding. The mention of "select tenures" suggests that the bank is specifically looking to fill gaps in its asset-liability matching, targeting specific maturity buckets to optimize its balance sheet.

The Broader "War for Deposits"

This rate hike occurs within the context of an industry-wide struggle for retail deposits. Across India, banks are experiencing a shift where credit growth is often outpacing deposit growth. This imbalance puts pressure on the Loan-to-Deposit Ratio (LDR), forcing banks to either slow down lending or seek more expensive funding sources. By raising FD rates, Bandhan Bank is attempting to bolster its CASA (Current Account Savings Account) and term deposit ratios, ensuring it has enough liquidity to support its lending operations without relying on volatile wholesale markets.

Macroeconomic Pressures and RBI Influence

The timing of this adjustment is closely linked to the broader monetary environment governed by the Reserve Bank of India (RBI). With inflation remaining a key concern, the RBI's stance on repo rates directly influences how commercial banks price their deposits. When the central bank maintains a high-interest-rate environment, retail investors become more discerning, moving their money toward institutions that offer the best risk-adjusted returns. Bandhan Bank's decision to hike rates is a proactive measure to prevent deposit flight to larger public sector banks or other aggressive private competitors.

Competitive Positioning Against Peers

In the competitive landscape of private banking, Bandhan Bank must differentiate itself from giants like HDFC or ICICI, which often have lower costs of funds due to massive existing deposit bases. For a mid-sized player, offering slightly higher rates is a classic market-penetration strategy. By undercutting or matching the top-tier rates of its peers, Bandhan Bank can attract "floaters"—depositors who move their funds based on incremental gains in interest. This strategy is essential for the bank to scale its operations and diversify its funding sources.

Future Implications for Retail Investors

Looking ahead, this trend of rising FD rates is likely to trigger a chain reaction among other private lenders. As Bandhan Bank raises the bar, other institutions may be forced to follow suit to protect their market share, potentially leading to a period of higher yields for retail savers. However, for the banks, this increase in the cost of funds will eventually need to be passed on to borrowers through higher lending rates to maintain Net Interest Margins (NIMs). This cycle underscores the delicate balance banks must maintain between attracting deposits and remaining profitable.

Conclusion

Bandhan Bank's decision to raise FD rates to 7.45% and 7.95% is a calculated move to strengthen its retail funding base in a highly competitive environment. By targeting senior citizens and specific tenures, the bank is addressing immediate liquidity needs while attempting to secure long-term stability. While this move increases the bank's interest expense, the benefit of a robust and diversified retail deposit base far outweighs the cost, ensuring the bank remains resilient amidst fluctuating economic conditions.

Verification Required?