Tripura woman reveals the financial reality of owning a Paris house beside ₹1.4 lakh EMI

Source Entity

Latest News: Today's Latest News Headlines from India & World | Hindustan Times | Hindustan Times

A Tripura woman broke down her Paris home expenses beyond her EMI, explaining why buying is still better than renting despite the extra costs.

Analysis of International Real Estate Investment: The Paris Home Ownership Case

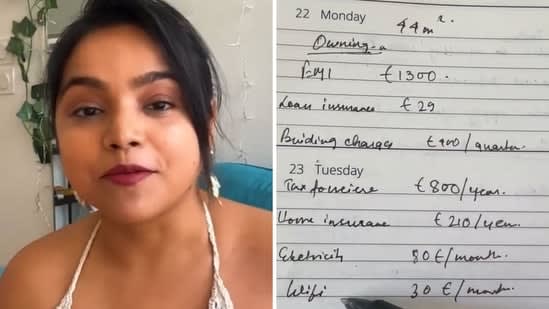

In a revealing account that has captured attention for its transparency, a woman from Tripura has detailed the financial intricacies of owning a residence in Paris, France. The core of her revelation centers on a monthly Equated Monthly Installment (EMI) of ₹1.4 lakh, but the narrative extends far beyond a simple loan payment. By breaking down the hidden costs associated with European property ownership, she provides a rare glimpse into the financial planning required for the Indian diaspora to maintain assets in one of the world's most expensive real estate markets.

The Financial Architecture of the Paris Property

The mentioned EMI of ₹1.4 lakh serves as the baseline for her monthly expenditure, but the analysis suggests that the 'true cost' of ownership involves several additional layers. In the French real estate system, owners are subject to the Taxe Foncière (property tax) and charges de copropriété (building maintenance fees), which can be substantial depending on the age and luxury level of the building. For an Indian investor, these costs are further complicated by the currency exchange rate between the Indian Rupee (INR) and the Euro (EUR), meaning that a fluctuation in the forex market can effectively increase or decrease the monthly burden even if the loan amount remains static.

The Strategic Logic: Buying vs. Renting in Paris

A critical component of this account is the woman's assertion that buying remains superior to renting. To understand this, one must look at the Paris rental market, which is notoriously competitive and characterized by high demand and limited supply. Renting in prime Parisian districts often yields zero equity, whereas a mortgage—even with a significant EMI—builds ownership in an asset class that historically appreciates. By opting for ownership, she is essentially converting a monthly expense into a long-term capital investment, hedging against the rising cost of living in France.

Socio-Economic Implications for the Indian Diaspora

This story highlights a shifting trend among Indians from diverse backgrounds, including those from smaller states like Tripura, who are now diversifying their portfolios into international prime real estate. Historically, overseas investments were the domain of ultra-high-net-worth individuals (UHNIs). However, the emergence of global mobility and remote work has made such investments more accessible. The ability to manage a ₹1.4 lakh EMI suggests a sophisticated approach to income generation and asset allocation, reflecting a broader trend of 'global citizenship' where wealth is distributed across different geographies to mitigate local economic risks.

Risks and Long-Term Sustainability

While the narrative champions ownership, it also implicitly warns of the financial discipline required. Maintaining a foreign property involves not just the EMI, but also insurance, utility costs, and the potential for vacancy if the property is not owner-occupied. The sustainability of such an investment depends heavily on the owner's ability to maintain a steady stream of income in a strong currency or a high-growth domestic career. For a resident of Tripura, managing a Parisian asset requires a high level of financial literacy and a strategic understanding of international tax laws to avoid double taxation.

Predicting Future Trends in Global Property Acquisition

Looking forward, we can expect more individuals from non-metropolitan Indian cities to seek real estate in European hubs. As the Indian economy grows, the desire for 'safe haven' assets in cities like Paris, London, or Berlin will likely increase. This trend will be driven by the desire for residency options, educational proximity for children, and the intrinsic value of European architecture and urban planning. The transparency provided by this woman's breakdown will likely encourage others to move beyond the 'glamour' of owning a home abroad and focus on the rigorous mathematical reality of mortgage management.

Conclusion

Ultimately, the account provided by the Tripura woman serves as a practical case study in international financial planning. By contrasting the ₹1.4 lakh EMI against the volatility and dead-cost of the Paris rental market, she makes a compelling argument for equity-building. Her experience underscores that while the entry barrier to the Parisian property market is high, the long-term financial rewards of ownership—coupled with the prestige and stability of the asset—outweigh the recurring costs of leasing.

Verification Required?